Update (April 2, 2018): Additional detail added for a more comprehensive look at managing disputes under the new VCR process.

Effective globally April 15, 2018

Visa recently announced its Visa Claims Resolution (VCR) initiative, designed to streamline and simplify the current Visa chargeback flow. The VCR initiative will restructure the dispute process from a litigation-based approach to a liability assignment process. This change will be implemented by Visa globally in April 2018. As the merchant account holder you’ll continue to dispute chargebacks via Braintree. Rest assured, Braintree will give you the tools you need to help manage these changes for your business.

The VCR was created with the following objectives:

- Improve chargeback-resolution time

- Reduce invalid disputes

- Define compelling evidence changes

- Simplify reason codes

Let’s look at each of these objectives a little more closely.

Improve chargeback-resolution time

Visa anticipates that changes to the required up-front information will help eliminate the back-and-forth between merchant, acquirer, and issuer, intending to result in a quicker chargeback resolution time for our merchants.

Due to the limitations as defined by the card networks’ mandate, you will no longer be able to submit additional evidence for any dispute case that has already been submitted, or for any case that has expired. There will be no exceptions. When the reply-by-date passes, Braintree will automatically respond to disputes with an “Accept” response and no further action can be taken. Upon receipt of each dispute case, we strongly suggest giving immediate attention to your cases to allow yourself appropriate time to submit evidence by the deadline.

We understand that managing and compiling evidence for dispute cases may require additional time now, and we'll be there to help you prepare for this shorter timeline.

Example:

Reply by date: May 11, 2018

This means that you have to either accept or submit evidence to the case by May 11 at 11:59pm (in your gateway time zone). Otherwise, the case will expire, you've forfeited your right to dispute, and the case will automatically be accepted.

Reduce invalid disputes

Each dispute will follow one of two workflows: allocation or collaboration. Below we’ll discuss more about how these will work and how they may impact the disputes received to your account.

Allocation

Fraud- and Authorization-related chargebacks would fall into the allocation bucket. Disputes that are managed under this category will be automatically processed by Visa, allowing them to reject disputes that don’t follow certain guidelines. These automated checks performed by Visa will look to answer the following questions:

- Was the dispute initiated within the allowed timeframe?

- Was the fraud dispute a 3D Secure-authorized transaction?

- Has the transaction been refunded?

If a dispute meets any of these criteria it can be blocked by Visa, preventing it from becoming a chargeback. This flow is expected to result in fewer invalid chargebacks. On the other hand, if the dispute is not deemed as invalid, Visa will assign liability to the merchant. Successfully defending these chargebacks will only be possible if you can definitively prove that the chargeback is invalid by providing compelling evidence. More on that later.

Visa anticipates as many as 60-80% of disputes will fall into the allocation bucket (fraud/not authorized). In this workflow, allocation dispute outcomes will be determined by CVV, AVS, and 3D Secure responses. If these tools are not enabled on your account, you will be liable for these disputes.

With this in mind, it also means there could potentially be an increase in fraud-to-sales ratios. In addition to monitoring chargebacks, the card associations also monitor reported fraud transactions with the Visa Fraud Monitoring Program (VFMP). See our post on VFMP to learn more. Visa is sunsetting dispute reason code 75 (Unrecognized), which was a reason code previously not considered fraud. With the VCR change, those “unrecognized” disputes will be placed into the fraud category which could impact fraud-to-sales ratios.

Collaboration

Collaboration will involve the same process as it does today, but is specifically associated with non-fraud related dispute reason codes. It requires interaction between merchants, processors, and issuing banks, but does not require compelling evidence to remedy the case.

The VCR initiative will help streamline the communication flow for collaboration disputes. You can find more details about our evidence recommendations for disputes that fall into this category in this post.

Compelling evidence changes

Certain reason codes require specific pieces of evidence to be provided in order to remedy a dispute. This is what we mean by “compelling evidence.” You can find more details about compelling evidence in this post.

Simplify reason codes

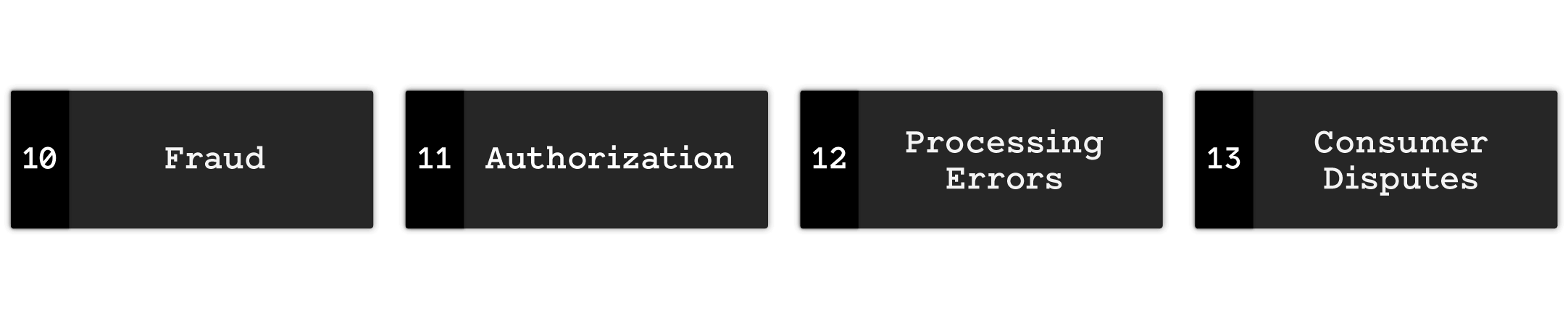

In addition to timeframe and workflow changes, Visa is consolidating its chargeback reason codes. Under the VCR initiative, the current chargeback codes will now be consolidated into four categories:

These new categories were created to reduce the complexity of the current dispute process as well as to hold card-issuing banks to certain standards. You can find more details about reason codes in this post.

What can these changes potentially mean for merchants?

- Quicker turnaround time on disputes

- Fewer cases to juggle

- Simplified reason codes

- Stricter rules around compelling evidence

How can merchants prepare?

- Standardize your documentation processes and familiarize yourself with compelling evidence requirements

- Promptly review and organize evidence needed to respond to disputes by the deadline

- Be proactive with chargeback and fraud mitigation

- Review and implement fraud tools (AVS, CVV, Advanced Fraud Tools, and 3D Secure)

- Update billing descriptors so that cardholders can easily recognize the charge

- Review and modify customer service practices as necessary to improve customer experience

- Promptly issue refunds

Looking for more information on reducing chargebacks and helping to prevent fraudulent transactions?

- Support article: Reducing Chargebacks

- Blog: How to Reduce Chargebacks: A Six Point Guide

- Support article: Braintree Fraud Tools Overview

If you have any questions please feel free to reach out to disputes@braintreepayments.com.

Source: Visa Claims Resolution